When you see a crypto exchange promising 40% APY on your deposits, it should raise alarms - not excitement. That’s exactly what BIB Exchange claims to offer, along with NFT minting, copy trading, and a "wealth box" for passive income. But behind the flashy numbers and slick website, there’s a darker story. The Washington State Department of Financial Institutions has issued a formal alert: BIB Exchange may have engaged in fraud. This isn’t a rumor. It’s an official government warning.

What Is BIB Exchange?

BIB Exchange says it’s a global crypto platform built on Binance Smart Chain, serving over 2 million users. It offers spot trading, futures, options, staking, and even an NFT marketplace. Its native token is $BIB, used for fees and rewards. On paper, it looks like a full-service exchange. But real users aren’t trading - they’re stuck.

The platform pushes high-yield products hard. The "Fund Investment" option promises 40% APY in USDT. "Easy Earn" gives 1.47% APY in BTC. "$BIB Pledge" offers 2.6% APY in $BIB. These returns aren’t just high - they’re impossible for any legitimate exchange to sustain without taking massive risk or outright lying. Compare that to Coinbase or Kraken, which offer 1-5% APY on stablecoins after rigorous audits. BIB’s numbers don’t just stretch credibility - they break it.

Regulatory Red Flags

BIB Exchange claims to hold a U.S. MSB license: #31000219137978. But here’s the catch: an MSB registration with FinCEN doesn’t mean it’s licensed to run a crypto exchange. It just means it registered as a money transmitter - a basic formality for any business handling cash. It says nothing about investor protection, market integrity, or withdrawal guarantees.

The real warning came from the Washington State Department of Financial Institutions (DFI). Their official alert named three domains: www.bibcoinltd.com, m.bibcoinltd.com, and www.bibvip.com (the main BIB Exchange site). They called out two specific crimes: Advanced Fee Fraud and Asset Recovery Scam. These aren’t minor issues. They’re criminal charges.

Advanced Fee Fraud means victims are asked to pay upfront fees - "taxes," "verification deposits," or "withdrawal charges" - before they can access their funds. Once paid, the money vanishes. Asset Recovery Scam happens after someone loses money on the platform. Then, a second group contacts them offering to "recover" their funds - for another fee. Both are classic signs of organized fraud.

Withdrawal Problems: The Smoking Gun

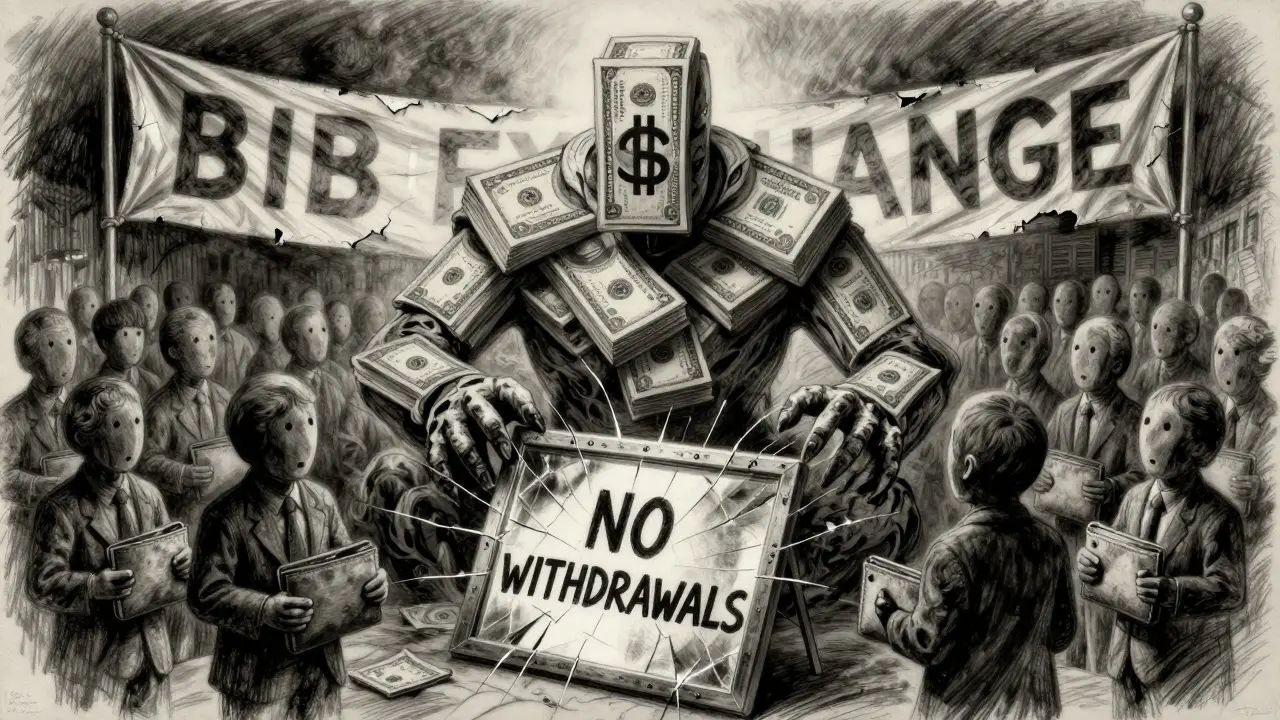

Legitimate exchanges let you withdraw. BIB Exchange doesn’t.

The Washington DFI received multiple complaints from users who tried to pull out their money - again and again - and couldn’t. One investor reported losing their entire deposit, plus years of "gains" they thought they’d earned. No refunds. No answers. No contact from support.

This isn’t a glitch. It’s the business model. Platforms that can’t or won’t let users withdraw are almost always scams. They rely on new deposits to pay "returns" to earlier users - a Ponzi structure. When new money dries up, the whole thing collapses. And when that happens, the operators disappear with the funds.

Compare this to Binance or Coinbase. Even during market crashes, they process withdrawals. They have insurance funds, cold storage, third-party audits, and legal teams. BIB Exchange has none of that. No public audit reports. No insurance disclosures. No jurisdictional clarity. Just a website and a promise.

Security Claims vs. Reality

BIB Exchange boasts "over 30 security layers": multi-layer wallets, DDoS protection, traffic cleaning, automatic risk systems. Sounds impressive, right? But security isn’t about flashy tech - it’s about access. If you can’t withdraw your money, your "security" is just a prison.

Real security means your funds are yours. Always. Even if the platform gets hacked, reputable exchanges have insurance and recovery protocols. BIB Exchange has no public proof of insurance. No history of audits. No transparency. The security claims are window dressing - meant to distract from the real problem: locked funds.

Why It’s Not on CoinMarketCap or CoinGecko

Legitimate exchanges are listed on CoinMarketCap and CoinGecko. These sites track trading volume, liquidity, and user activity. If a platform isn’t there, it’s not being monitored by the industry.

BIB Exchange doesn’t appear on either. Why? Because it doesn’t meet basic listing criteria. No verifiable trading volume. No liquidity data. No API access. That’s not an oversight - it’s a red flag. You can’t fake volume on these platforms. They require audits, proof of reserves, and real user data. BIB Exchange has none of that.

How It Compares to Legitimate Exchanges

| Feature | BIB Exchange | Legitimate Exchanges (e.g., Coinbase, Kraken) |

|---|---|---|

| APY on Stablecoins | Up to 40% (USDT) | 1-5% |

| Regulatory Oversight | Claims MSB registration only | Licensed in multiple jurisdictions (e.g., NYDFS, FCA) |

| Withdrawal Reliability | Users report being blocked | Withdrawals processed within 24-72 hours |

| Third-Party Audits | No public reports | Regular audits by firms like CoinCheckup or CertiK |

| Insurance Fund | Not disclosed | Yes (e.g., Coinbase holds $250M+ in insurance) |

| Listing on CoinMarketCap/CoinGecko | No | Yes |

| Government Fraud Warning | Yes (Washington State DFI) | No |

What Experts Say

Cryptocurrency security researchers and former regulators agree: if a platform has a government fraud alert and restricts withdrawals, don’t touch it. The Washington DFI’s warning is one of the strongest signals you can get. It’s not a rumor. It’s not a blog post. It’s a formal, legally backed consumer alert.

Financial experts also point out that BIB Exchange’s structure matches known scam patterns: high returns to lure victims, fake security claims to build trust, and withdrawal blocks to trap funds. Once you deposit, you’re not a customer - you’re a source of cash.

Current Status (March 2026)

As of early 2026, BIB Exchange is still operating. Its website is live. Its Telegram groups are active. It’s still pushing those 40% APY offers. But it’s also still under investigation.

There’s no evidence it’s shut down. There’s also no evidence it’s safe. The Washington DFI hasn’t retracted its warning. No other regulator has endorsed it. No user has successfully withdrawn large sums publicly.

If you’re thinking of depositing money here - don’t. Even if you "earn" a few hundred dollars in fake rewards, you’ll lose everything when the platform shuts down - and it will. The only people winning are the operators.

What to Do Instead

Stick to platforms that are:

- Licensed by major regulators (e.g., SEC, FCA, ASIC)

- Listed on CoinMarketCap and CoinGecko

- Transparent about audits and insurance

- Offer APY under 10% for stablecoins

- Let you withdraw without delays or fees

Examples: Coinbase, Kraken, Bitstamp, Gemini. These aren’t flashy. They don’t promise moonshots. But they’ve been around for years. They’ve survived crashes. They’ve passed audits. And most importantly - they let you get your money out.

If you’ve already deposited into BIB Exchange, stop sending more money. Document every transaction. Contact your local financial regulator. Report it to the Washington DFI. And prepare for the possibility that you won’t get your funds back. It’s not a risk - it’s a loss waiting to happen.

Is BIB Exchange a scam?

Yes, based on official government warnings. The Washington State Department of Financial Institutions has labeled BIB Exchange as potentially fraudulent, citing Advanced Fee Fraud and Asset Recovery Scam patterns. Users report being unable to withdraw funds, which is a hallmark of crypto scams. There is no verified evidence that BIB Exchange is legitimate.

Can I trust BIB Exchange’s 40% APY?

No. No legitimate crypto exchange offers 40% APY on stablecoins. The highest rates on platforms like Coinbase or Kraken are under 5%. Anything above 10% is unsustainable and almost always a red flag for a Ponzi scheme. BIB’s 40% APY is designed to attract new deposits to pay earlier users - not to generate real returns.

Why isn’t BIB Exchange on CoinMarketCap?

CoinMarketCap and CoinGecko require exchanges to prove real trading volume, liquidity, and transparency through audits and API access. BIB Exchange doesn’t meet these standards. Its absence from these platforms isn’t an oversight - it’s proof that it doesn’t operate like a real exchange.

What should I do if I already deposited into BIB Exchange?

Stop depositing more money. Document all transactions, including dates, amounts, and screenshots of withdrawal attempts. Contact your local financial regulator and report the platform to the Washington State DFI. Unfortunately, recovery is unlikely - most users in similar cases never get their funds back. Treat any money sent as lost.

Does BIB Exchange have a license?

BIB Exchange claims to hold a U.S. MSB license (#31000219137978), but an MSB registration only means it registered as a money transmitter - not that it’s licensed to operate a crypto exchange. It does not provide investor protection, audit compliance, or withdrawal guarantees. No major regulator (SEC, FCA, ASIC) recognizes BIB Exchange as legitimate.

Final Verdict

BIB Exchange isn’t a crypto exchange. It’s a high-yield trap. The 40% returns? A lure. The security claims? A distraction. The withdrawal blocks? The trapdoor. The Washington DFI didn’t issue a warning by accident. They did it because real people lost real money. And they’re still losing it.

If you’re looking to trade crypto, use a platform with a track record. Not one with a flashy website and a government fraud alert. Your money deserves better than a gamble with criminals.

Wow. Just... wow. I read this whole thing and I’m not even mad, I’m just disappointed. Like, how do people still fall for this? The 40% APY isn’t even the worst part-it’s the way they make it look so legit with fake security layers and that MSB license bluff. It’s like watching someone try to sell a fake Rolex in a Walmart parking lot and calling it "artisanal craftsmanship."

If you’re thinking about putting money into BIB, stop. Just stop. I’ve seen this movie before-high returns, locked withdrawals, fake audits. It’s always the same script. The Washington DFI didn’t issue that warning for fun. They’re protecting real people. Don’t be the next statistic. Walk away now. Your future self will thank you.

And if you already deposited? Document everything. screenshot every error message. You might not get your money back, but at least you’ll have proof when the feds finally move.

🇺🇸 #AmericaFirst #NoMoreScams

Any individual considering depositing funds into this entity is at extreme risk of total capital loss and should immediately cease all engagement.

It’s not a delay. It’s a coffin. Please. If you’re reading this and you’re still thinking about it… don’t. You won’t regret walking away. But you’ll regret putting your life savings in a black hole.

💔

There’s a philosophical paradox here, isn’t there? We live in a world where value is increasingly abstract-digital tokens, algorithmic yields, decentralized trust. And yet, the oldest human flaw remains: the hunger for effortless abundance. BIB Exchange doesn’t offer crypto. It offers a mirror. And in that mirror, we see our own desperation to believe in magic.

The 40% APY isn’t a financial product. It’s a psychological trap. A siren song sung by the same forces that once sold snake oil and moonshine. The platform is a symptom, not the cause. The real fraud is the belief that we can escape the laws of physics, economics, and time.

Withdrawal blocks? They’re not bugs. They’re the final act of a tragedy written in our own greed.

It’s not about BIB. It’s about the system. The system lets this happen. The system lets people make websites that look like banks. The system lets them use terms like "stake," "yield," "APY"-words borrowed from legitimate finance-and weaponizes them. The regulators don’t stop it because they’re underfunded. The media doesn’t cover it because it’s not viral enough. The users don’t learn because they’re addicted to the dopamine hit of fake gains.

So who’s really at fault? The scammers? Or the society that raised them? We don’t need more warnings. We need better education. Or better yet-we need to stop pretending that financial literacy is optional.

Do not engage. Do not deposit. Do not rationalize. This is not an investment. It is a liability waiting to be liquidated.

I mean… I get it. I really do. I used to be the person who thought "if it’s too good to be true, it’s probably a scam" was just a phrase people said to feel smart. Then I lost my entire crypto portfolio in 2021 to a "decentralized yield farm" that promised 200% monthly returns. I thought I was being clever. I thought I was ahead of the curve. I thought the blockchain was magic.

It’s not magic. It’s math. And math doesn’t care how hard you believe in it.

BIB isn’t just a scam. It’s a mirror of every bad decision I ever made. The late-night research. The FOMO. The "just one more deposit" mentality. The way I convinced myself that if I just waited a little longer, the system would fix itself.

It won’t. It never does.

I don’t post often. But I had to say this. If you’re reading this and you’re still thinking about it… don’t. You’re not smarter than the system. You’re just one more data point in their profit margin.

From India, I just want to say: this is not unique to the US. We have seen the same patterns here-fake platforms promising 50% monthly returns, fake KYC, fake withdrawal systems. The language changes, but the scam doesn’t. I’ve spoken to three families who lost everything. One person even sold their home. We need more awareness. Not just in the US, but everywhere. Crypto is powerful. But it’s not magic. And no one who truly understands finance would ever promise 40% APY on USDT.

Thank you for writing this. It’s a lifeline for people like me who are trying to protect others.

From a compliance and risk management standpoint, the structural indicators here align with high-risk financial intermediation profiles. The absence of verifiable liquidity, the reliance on tokenized yield mechanisms without underlying asset backing, and the use of regulatory terminology (MSB) to create false legitimacy are all consistent with known fraudulent architectures. Furthermore, the psychological anchoring effect of "40% APY" as a cognitive hook-paired with the normalization of NFT minting and copy trading as value-add features-creates a multi-layered deception ecosystem. This is not a rogue actor. This is a systematized predatory model. The Washington DFI alert is not merely reactive-it is prophylactic. Any engagement constitutes material exposure to irreversible capital loss.