You hold Bitcoin on a foreign exchange like Binance or KuCoin. Your portfolio value just hit $15,000. Suddenly, you remember hearing about the FBAR, which is the Foreign Bank and Financial Account Report required by US persons holding foreign financial accounts exceeding $10,000. Panic sets in. Do you need to file? Will the IRS come after you?

The short answer is complicated. As of May 2026, the rules for reporting foreign cryptocurrency accounts are still shifting. For most people with pure crypto holdings, the immediate requirement might be 'no.' But if you hold fiat currency alongside your tokens, or if you take a conservative approach to risk, the answer changes completely. This guide cuts through the noise and explains exactly where you stand.

What Is the FBAR and Who Must File?

The FBAR stands for Foreign Bank and Financial Account Report. It is not an IRS form. It is filed with FinCEN, which is the Financial Crimes Enforcement Network, a bureau of the US Treasury Department. The purpose is straightforward: the government wants to know about money sitting outside the United States.

You must file FinCEN Form 114 if you are a US person (including citizens, residents, and entities like LLCs) and you have a financial interest in or signature authority over foreign financial accounts. The trigger is simple: if the aggregate value of all these accounts exceeds $10,000 at any single point during the calendar year, you have a filing obligation. This is not an average. If your account hits $10,001 on March 15 because Bitcoin spiked, you report it.

The deadline is October 15 of the following year. For example, for the 2025 tax year, you must file by October 15, 2026. Unlike many other tax forms, there is no automatic extension, though you can request a six-month extension under specific circumstances.

The Crypto Loophole: FinCEN Notice 2020-2

Here is where things get tricky for crypto holders. In December 2020, FinCEN issued Notice 2020-2, which is a regulatory guidance stating that foreign accounts holding only virtual currency are not currently reportable on the FBAR. This notice remains effective as of 2026.

This means if you have an account on a foreign exchange like Binance.com or KuCoin and it contains only cryptocurrencies (Bitcoin, Ethereum, Solana, etc.), you technically do not need to include it in your FBAR filing right now. The exemption applies because FinCEN has not yet updated its regulations to explicitly define virtual currency accounts as 'reportable' under the current code.

However, this is a temporary status. FinCEN has stated clearly in Notice 2020-2 that they intend to propose amendments to include virtual currency in future rules. Many experts believe this change could happen within the next 1-2 years. Relying on this loophole long-term carries risk, especially if new rules apply retroactively or lack safe harbor provisions for past non-filing.

The Hybrid Account Trap

The biggest mistake crypto investors make is assuming their entire exchange account is exempt. Most trading platforms allow you to deposit fiat currency (USD, EUR, GBP) to buy crypto. If your foreign account holds any traditional currency alongside your digital assets, it becomes a 'hybrid account.'

Hybrid accounts are fully reportable. FinCEN Notice 2020-2 explicitly states that an account is reportable if it holds reportable assets besides virtual currency. So, if you have $8,000 in Bitcoin and $3,000 in Euros sitting in your Binance wallet, the total value is $11,000. Because part of that value is fiat, the entire account is subject to FBAR reporting if it crosses the $10,000 threshold.

To stay compliant, you must track your account composition daily. A spike in crypto prices might push your total value over $10,000, but if you withdraw all fiat funds before that spike, you might remain exempt. However, once fiat re-enters the account, the clock resets.

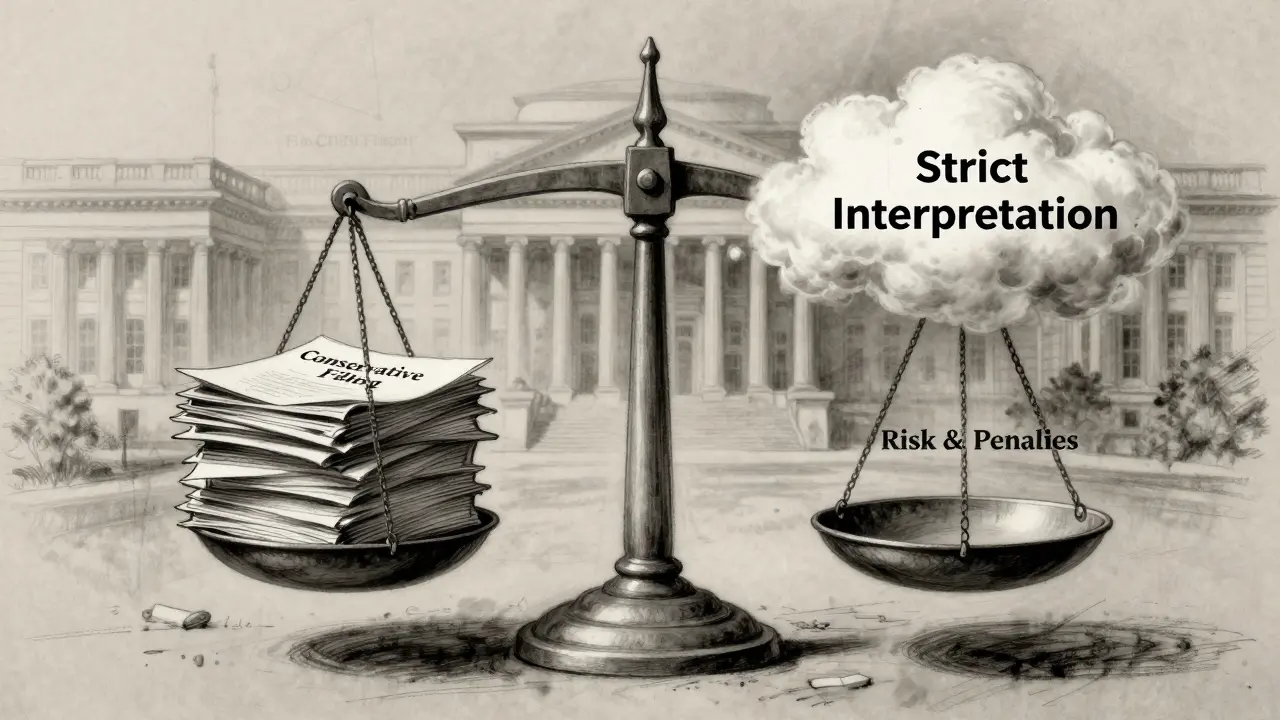

Conservative vs. Strict Compliance Strategies

Tax professionals are divided on how to handle this uncertainty. There are two main camps:

- The Conservative Approach: Advocated by firms like CoinLedger and Jordan Bass, Head of Tax Strategy. They recommend filing the FBAR for foreign crypto accounts exceeding $10,000 even if they are pure crypto. Why? To mitigate risk. If FinCEN changes the rules tomorrow, you already have a history of compliance. This avoids penalties and potential audits. It treats the exemption as a grace period, not a permanent rule.

- The Strict Interpretation Approach: Supported by specialists like Bitwave. They argue that FinCEN Notice 2020-2 is clear: pure crypto accounts are not reportable now. Filing them creates unnecessary administrative burden and potentially flags your return for review without legal benefit. They advise waiting for final regulations before expanding reporting obligations.

Which path should you choose? If you are an individual with modest holdings, the strict approach might save you time. If you are an institutional investor, a corporate treasury, or someone with significant exposure to multiple foreign exchanges, the conservative approach offers peace of mind. Remember, the penalty for willful failure to file can be up to $10,000 or 50% of the account balance, whichever is greater.

How to Calculate Your Aggregate Value

Calculating the value of volatile crypto holdings for FBAR purposes is challenging. You need the maximum aggregate value of all foreign accounts at any single point during the calendar year. Here is how to do it correctly:

- Identify All Foreign Accounts: List every platform outside the US where you hold assets. This includes centralized exchanges (CEX), decentralized finance (DeFi) protocols if they involve custodial elements, and foreign brokerage accounts.

- Determine Daily Balances: You must convert your crypto holdings to USD equivalents for each day of the year. Use reliable data sources like CoinMarketCap or CoinGecko for historical prices.

- Find the Peak: Identify the highest total value across all accounts on any single day. If Account A peaked at $9,000 on Jan 10 and Account B peaked at $9,000 on Feb 20, but both held $5,000 simultaneously on March 5, your aggregate peak is $10,000. You report the highest simultaneous value.

- Include Fiat: Add any USD, EUR, or other fiat balances held in those accounts at the time of the peak.

Specialized crypto tax software can automate this process. Manual spreadsheets are error-prone and difficult to defend in an audit. Ensure your software tracks foreign exchange rates accurately.

| Account Type | Assets Held | Value > $10k? | Reportable on FBAR? |

|---|---|---|---|

| Pure Crypto Exchange | Only BTC, ETH, etc. | Yes | No (per Notice 2020-2) |

| Hybrid Exchange | Crypto + USD/EUR | Yes | Yes |

| US-Based Exchange | Crypto + Fiat | Yes | No (Not Foreign) |

| Foreign Brokerage | Stocks + Crypto | Yes | Yes |

Filing Process and Penalties

If you decide to file, you must use the BSA E-Filing System. You cannot mail paper forms. Individual filers register directly, while tax preparers must register as authorized e-file providers. The system requires specific details: the name and address of the foreign financial institution, the account number, and the maximum value during the year.

Getting accurate information from privacy-focused exchanges can be difficult. Some platforms do not provide standard account numbers or physical addresses. In these cases, document your best effort and keep records of correspondence with the exchange. Ignorance is not a valid defense for non-compliance.

Penalties for non-filing are severe. Non-willful violations can result in a $10,000 fine per violation. Willful violations-where you knowingly ignore the requirement-can lead to fines of up to $10,000 or 50% of the account balance, plus criminal charges. Given the ambiguity around crypto, the IRS and FinCEN have shown some leniency, but this window is closing. Proactive compliance is always safer than reactive defense.

What About Form 8938?

Don't confuse FBAR with Form 8938, which is the Statement of Specified Foreign Financial Assets filed with the IRS. Form 8938 has higher thresholds ($50,000-$75,000 depending on residency and filing status) and different rules. Currently, virtual currency is generally not considered a specified foreign financial asset for Form 8938 unless it is held in a foreign financial account that is otherwise reportable. However, the IRS has indicated it may update these rules in the future. Always check both FBAR and Form 8938 requirements separately.

Do I need to file FBAR if my crypto is only on Coinbase?

No. Coinbase is a US-based financial institution. FBAR only applies to foreign financial accounts. If your account is registered in the United States, it does not count toward the FBAR threshold, regardless of whether it holds crypto or fiat.

What if my crypto account dropped below $10,000 for most of the year?

You still need to file if it exceeded $10,000 at any single point during the calendar year. The threshold is based on the maximum aggregate value, not the average or end-of-year balance. Even one day over $10,000 triggers the requirement.

Is FinCEN Notice 2020-2 still valid in 2026?

Yes, as of May 2026, Notice 2020-2 remains effective. It continues to exempt pure foreign cryptocurrency accounts from FBAR reporting. However, FinCEN has signaled intent to update regulations, so this exemption could change soon. Monitor official announcements for updates.

Can I claim the innocent spouse relief for FBAR penalties?

FBAR is a joint liability for married couples filing jointly. Innocent spouse relief is rarely granted for FBAR violations because the law requires both spouses to be aware of the foreign accounts. If one spouse hides accounts, the other may still be liable. Consult a tax attorney for specific cases.

Do DeFi wallets count as foreign financial accounts?

Generally, no. Self-custody wallets (like MetaMask or Ledger) where you hold the private keys are not considered financial accounts maintained by a third-party institution. FBAR applies to accounts held with foreign banks or exchanges. However, if you use a custodial DeFi service located outside the US, it may qualify as a reportable account.